The Casita is a folding house made of 361 square feet of steel-skinned, foam-filled, magnesium-oxide-boarded American optimism, folded down to 8.5 feet wide and trucked out to a parking lot somewhere in Nevada to await the buyers who will finally make Boxabl a real company. Boxabl sells it for $60,000. In all of 2025, the company delivered 23 of them.

On June 9, the shareholders of FG Merger II Corp will vote on combining Boxabl with their SPAC at an enterprise value of $3.5 billion.

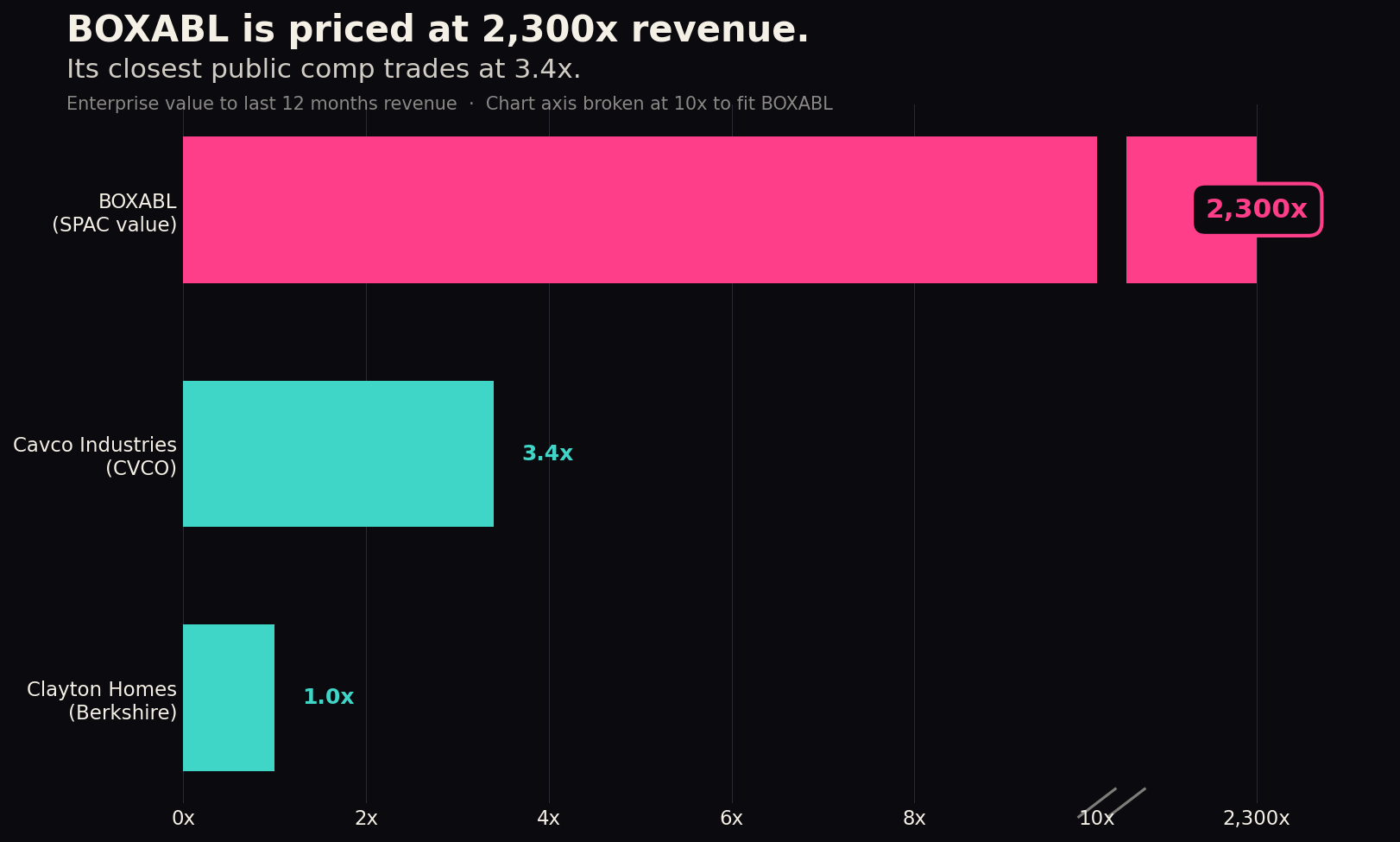

That works out to about 2,300 times revenue. Cavco Industries, the publicly traded manufactured-housing comp closest to Boxabl's business, trades at roughly 3.4 times. The valuation is the strangest number in a filing full of strange numbers, and the filing is where this story lives.

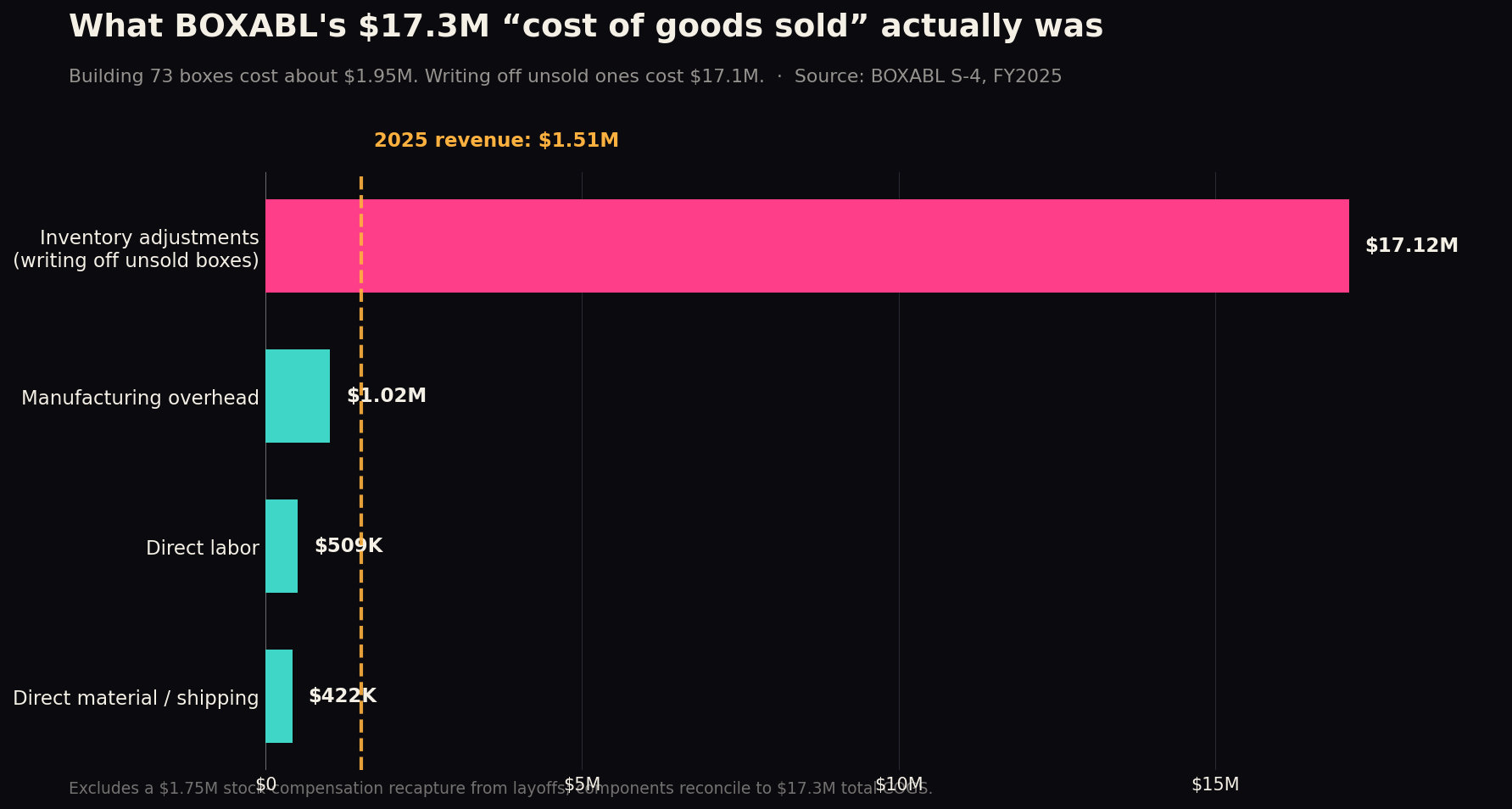

According to Boxabl's S-4 registration statement, the company recorded $1.51 million in revenue in 2025, down 55 percent from the year before. Cost of goods sold was $17.3 million. The filing's breakdown shows that only $1.9 million of that was the actual cost of materials, labor, and overhead for the 73 boxes the factory produced. The remaining $15.4 million was inventory write-downs. The company spent roughly $2 million building boxes last year and $15 million writing off boxes it could not sell.

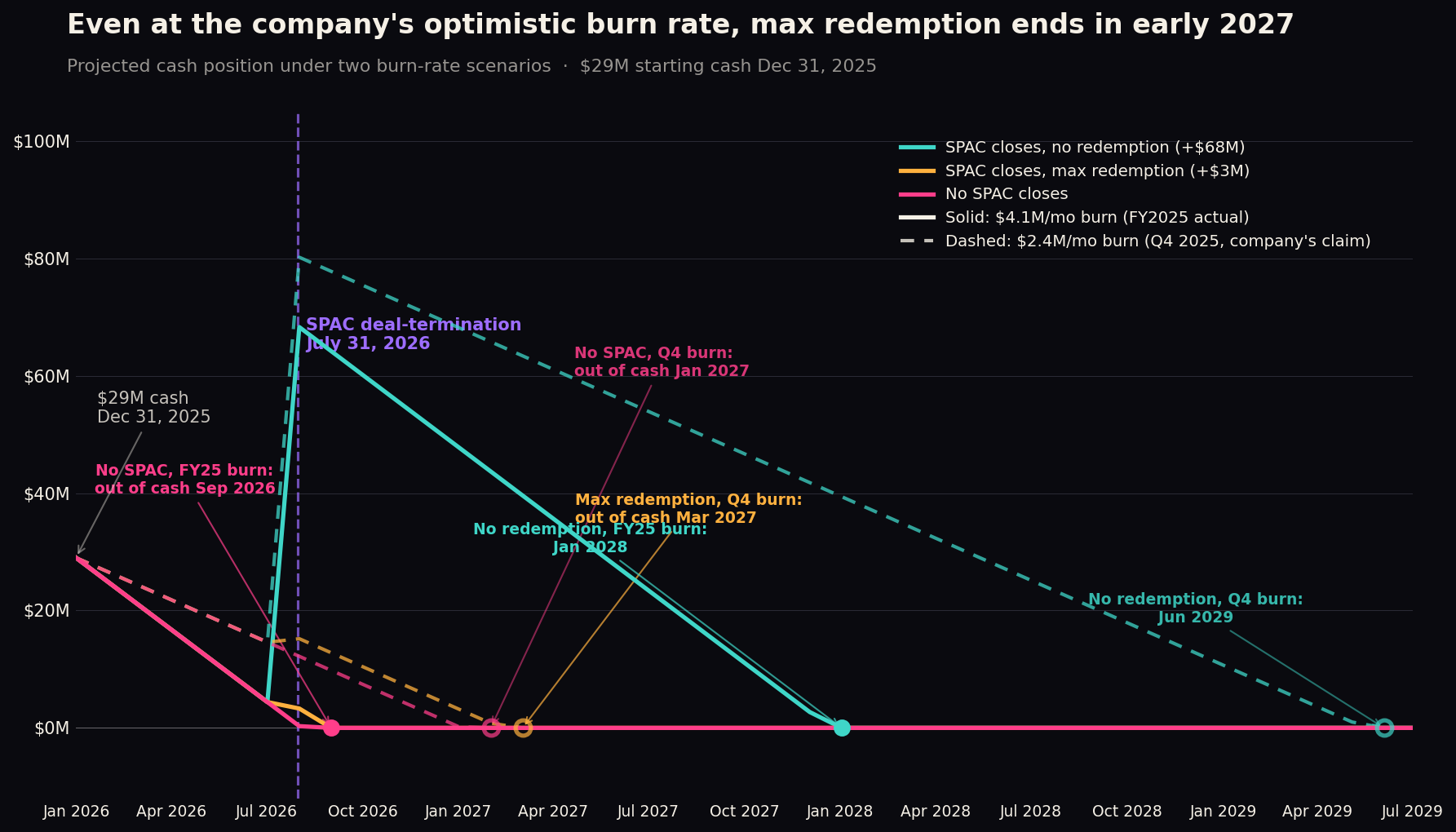

The losses are not new. Boxabl says it has raised more than $230 million from over 50,000 investors since 2017, mostly through Reg A+ and Reg D crowdfunding rounds. At year-end 2025, $29 million of that remained. The auditors issued a going-concern opinion. The company's operating cash burn was $33 million in 2023, $38 million in 2024, and $47 million in 2025, an acceleration the company attributes in part to scaling, in part to one-time charges. Q4 2025 burn ran at $2.4 million a month. The full-year average ran at $4.1 million a month. At either rate, the runway is measured in months, not years.

The SPAC's deal-termination deadline is July 31, 2026.

The merger agreement, according to the filing, contains no minimum cash condition. FGMC shareholders are entitled to redeem their public shares for roughly $10 a share before closing, regardless of how they vote. The trust holds about $82 million. If redemptions are heavy, Boxabl gets a Nasdaq listing, a fresh slate of public-company compliance obligations, and not much else. The filing's own modeling includes a "Maximum Redemption Scenario" in which the trust is fully drained.

The governance picture matches the financial one. Paolo Tiramani is CEO. His son Galiano is co-CEO. Both draw $595,000 salaries, identical to the dollar. Until June 2023, the patents underpinning the business were held personally by Paolo through a vehicle called Build IP LLC, which the company then merged into Boxabl at a $30 million valuation it assigned itself, paid in stock, with no independent appraisal disclosed.

In December 2025, with the going-concern opinion in place and the merger proxy weeks from filing, Galiano licensed the company's trademarks back to himself personally to launch a Boxabl-branded cryptocurrency meme coin. The board approved the deal. Boxabl is to receive royalties equal to gross cash flows less expenses.

Four of Boxabl's independent directors resigned in the twelve months before the vote. The company replaced one. FGMC did not commission an independent fairness opinion on the $3.5 billion price, and the filing states this plainly. The valuation, the same filing explains, was derived from Boxabl's own most recent crowdfunding round.

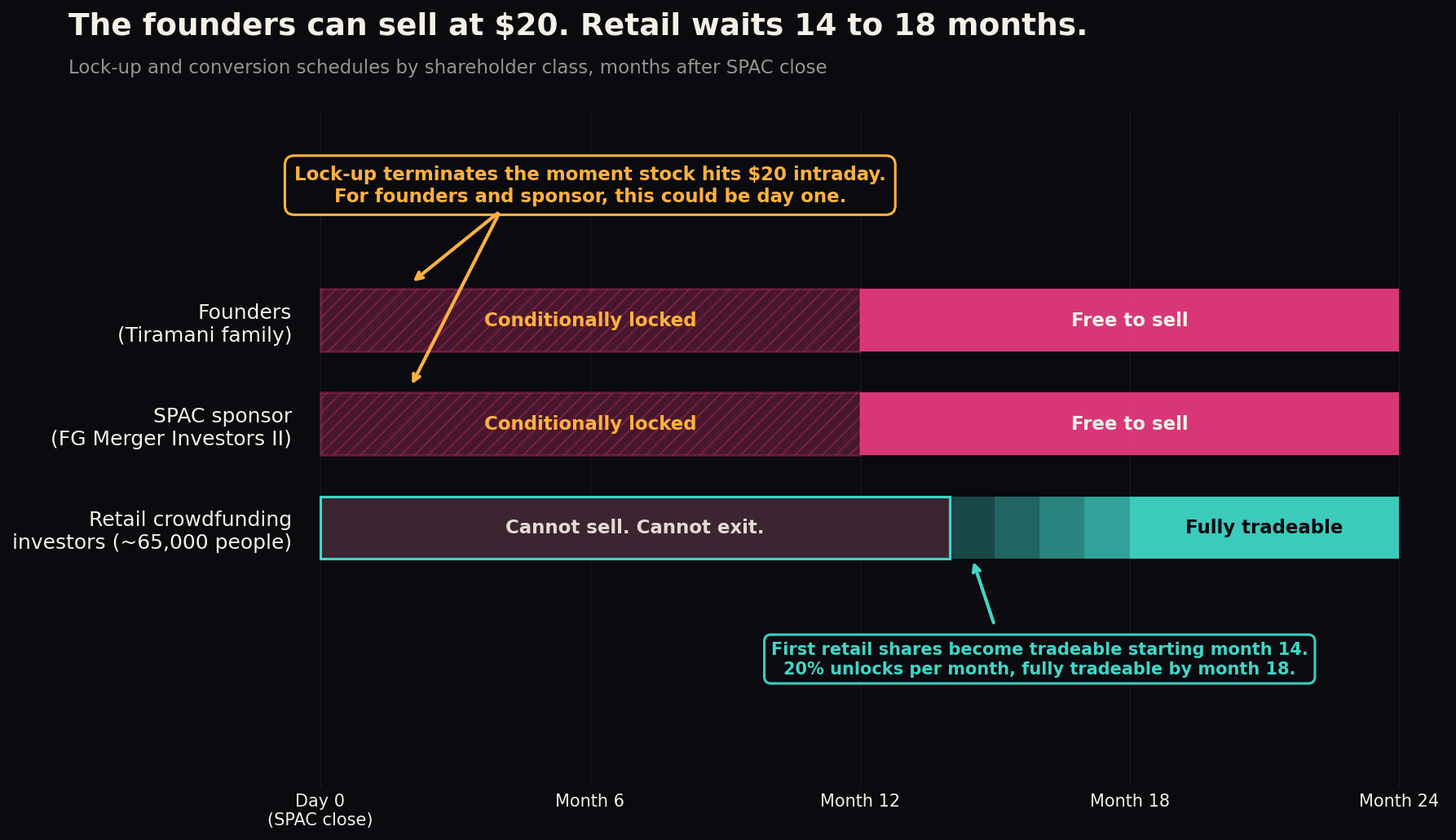

For the 50,000 retail investors, the deal mechanics are worse than the price. Most do not own common stock. They own Series A-3 Preferred, bought at $0.80 a share. The merger converts each old preferred share into roughly 0.078 shares of new Merger Preferred, deemed at $10. The new instrument is not listed on any exchange. The common stock will trade as BXBL on Nasdaq but the preferred will not. Conversion to tradeable common begins in month 14 after closing and finishes in month 18.

If the deal closes August 1, 2026, retail's first tradeable share arrives in October 2027. Full liquidity in February 2028.

The lock-up on Paolo, Galiano, and the FGMC sponsor terminates automatically the first time the combined company's stock prints at or above $20, intraday, at any time. The SPAC entry price is $10. The founders and the sponsor are therefore free to sell into a 2x move. The retail investors who provided the capital are locked into an unlisted security through eighteen months of post-merger trading they cannot participate in. By the time their shares become tradeable, the people who hold most of the post-merger equity will have had every opportunity to leave.

Some perspective on what a $3.5 billion actually means here. To grow into the valuation at a public-comp multiple of 3-5x revenue, Boxabl would need to ship somewhere between 23,000 and 58,000 Casitas a year. It shipped 23 last year.

Cavco runs 33 production lines to ship roughly 20,000 manufactured homes annually. Boxabl runs one line, at about six percent of its own stated capacity, in a single Nevada factory. A realistic bull case looks like Boxabl reaching 500 units a year by 2028, securing additional state approvals, and getting acquired by a strategic buyer like D.R. Horton, Lennar, or a Berkshire subsidiary at a 3-5x revenue multiple.

That bull outcome implies an enterprise value somewhere between $150 and $500 million, which is still a 90 percent loss from the SPAC entry price. The bear case, in which the trust is largely redeemed, Boxabl runs out of cash in 2027, and the company restructures or sells at distressed prices, implies an enterprise value of $10 to $30 million. A 99 percent loss.

The realistic outcomes, in my opinion, cluster well below the entry price. The outcome that would justify the entry price requires believing this management and this balance sheet will execute a fifteen-year plan they have so far missed by light years.

The vote is June 9. The deadline is July 31 by which the deal closes or not. Either way, I think this box folds.

A note on method and sourcing. All financial figures, dates, share counts, and corporate facts in this article are drawn from Boxabl Inc.'s and FG Merger II Corp.'s public filings with the U.S. Securities and Exchange Commission, principally the Form S-4/A registration statement, except where another source is named. Production-target comparisons referencing the company's projections rely on contemporaneous third-party descriptions, noted where used. Valuations, scenario probabilities, loss estimates, and characterizations of the transaction are the author's analysis and opinion, not statements of fact. Reasonable people may weigh the same filings differently. Nothing here is a prediction of how any security will trade. This article is journalism and commentary. It is not investment, legal, tax, or financial advice, and it is not a recommendation to buy, sell, hold, or vote any security. The author holds no position in any security mentioned. Readers should consult the primary filings and their own advisors before making any decision. Research and drafting for this article were assisted by AI tools which can make mistakes. As an investor and analyst, I also make mistakes and am often wrong in my analysis and predictions.