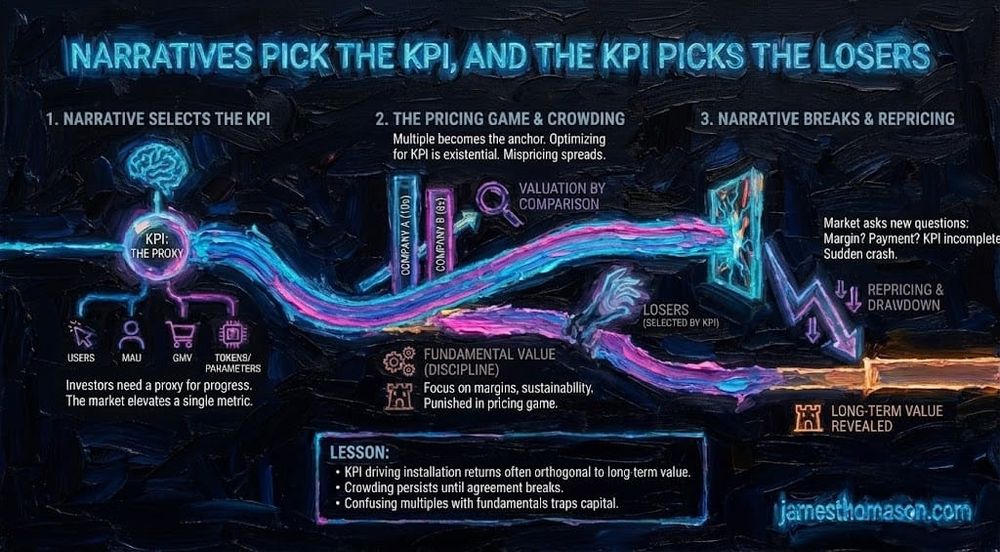

In every technology cycle, investors look for a number that feels like progress. Something observable, comparable, and plausibly connected to future cash flows. That number becomes the key performance indicator of the era.

At first, the choice feels reasonable. Early in a market’s life, revenues are small, margins are unstable, and business models are still forming. Traditional valuation tools struggle. A proxy is needed. So the market elevates a KPI that seems closest to value creation.

Users in the early internet.

Monthly active users in social media.

Gross merchandise volume in e-commerce.

Tokens served and model parameters in AI.

Once selected, that KPI does far more than describe the business. It becomes the organizing principle of valuation. And once that happens, it begins to select winners and losers in ways that have very little to do with eventual profitability.

The pricing game begins when investors stop asking what a company will earn and start asking how it compares to its peers. If Company A trades at ten times users and Company B trades at eight times users, the conclusion is not that users are a weak proxy. The conclusion is that Company B is cheap.

The multiple, not the cash flow, becomes the anchor.

This is how collective mispricing spreads across a sector. Each company may look only slightly stretched relative to its peers, but the entire cohort drifts further and further away from fundamentals together. The crowding gap described in the prior essay is the arithmetic consequence of this process. The pricing game is the behavioral mechanism that produces it.

Narratives choose the KPI because narratives answer the question investors are really asking in installation phases. Not “how much money will this make,” but “what is the right way to measure progress before the money arrives.”

The problem is that the KPI that best signals progress early is rarely the one that predicts who will win later.

User growth rewards companies that subsidize adoption. GMV rewards companies that move volume without regard to margin. Tokens served reward scale of computation, not efficiency or willingness to pay. Each of these metrics can be maximized in ways that actively harm long-term economics.

Yet once a KPI becomes the narrative focal point, firms are forced to optimize for it. Not because management is irrational, but because capital markets are. When valuations, compensation, and access to funding are tied to a single metric, deviating from it becomes existentially risky.

This is where losers are chosen.

The companies that ultimately dominate a sector are often the ones that look worse on the prevailing KPI during installation. They grow more slowly. They focus on integration, reliability, cost control, or enterprise fit. They trade narrative momentum for operational discipline. In the pricing game, that discipline is punished.

History is full of examples. The dot-com era rewarded traffic and page views. Amazon looked expensive and unprofitable relative to peers that optimized for eyeballs. Social media rewarded MAUs. Companies that focused on monetization early looked inferior until the narrative flipped. In online advertising, impressions and click-through rates mattered until margins and pricing power suddenly did.

AI is repeating the pattern. Tokens served, model size, and benchmark scores have become the dominant KPIs. They are easy to measure and easy to compare. They feel like progress. But none of them guarantee willingness to pay, sustainable margins, or defensible differentiation.

Once these KPIs drive valuation, the pricing game takes over. Investors stop underwriting businesses and start underwriting relative position in the cohort. Capital flows toward the companies that look best on the chosen metric, regardless of whether that metric maps to future cash flows.

This is why mispricing becomes synchronized. Everyone is using the same ruler.

Cornell and Damodaran emphasize that this is not stupidity or fraud. It is coordination. In early markets, pricing off peers is safer than pricing off uncertain fundamentals. No one wants to be wrong alone. The result is a market that is internally consistent and externally disconnected from reality.

Eventually, the narrative breaks. Not because the KPI was meaningless, but because it was incomplete. The market begins to ask different questions. Not how many users, but how much they pay. Not how much volume, but at what margin. Not how many tokens, but who bears the cost of serving them.

When the KPI changes, the leaderboard changes with it.

This is the most underappreciated source of drawdowns in technology cycles. Valuations do not fall because growth stops. They fall because the metric that defined success stops being the one that matters.

This is uncomfortable. During installation, the KPI that drives returns is often orthogonal to the KPI that determines long-term value. Playing the pricing game can be profitable, but only if you recognize it as such. Confusing KPI-driven multiples with fundamentals is how capital gets trapped when narratives turn.

This also explains why crowding persists longer than arithmetic suggests it should. As long as the KPI remains credible, the pricing game sustains itself. Numbers keep going up because the market agrees on what to measure.

When that agreement breaks, repricing is sudden and brutal.